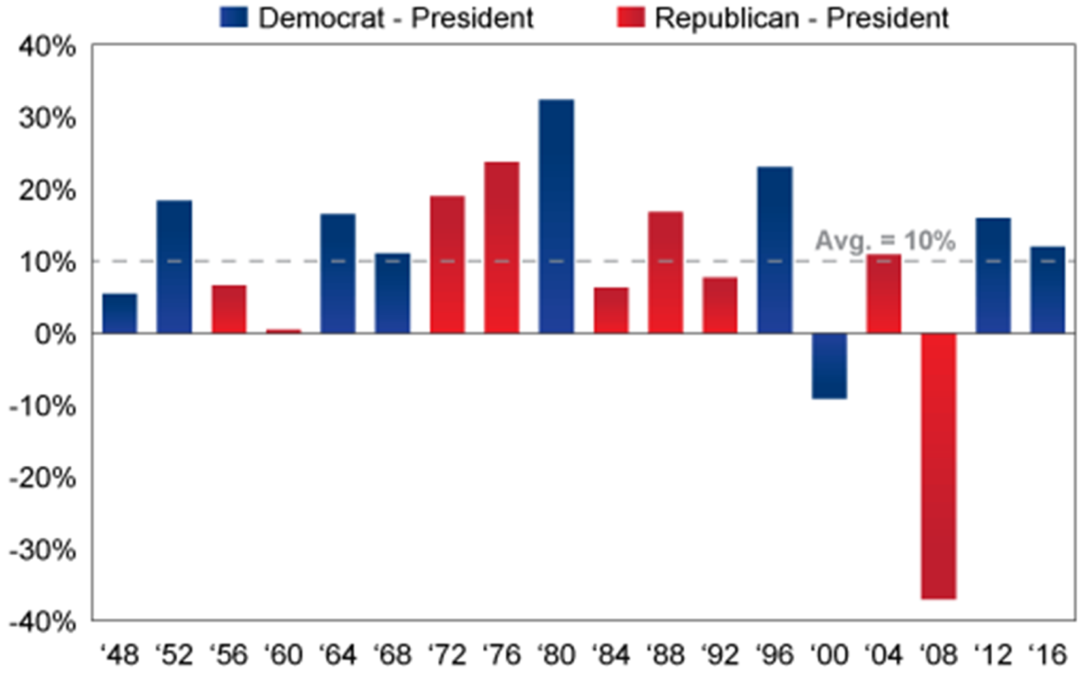

A common question I’ve heard as of late is ‘what’s the stock market going to do given the upcoming election?’ Well let’s start by looking at how the S&P 500 has fared in the 18 elections since World War II.

There has only been 2 years out of the 18 where the market ended down (so only 11.11% of election years). One was under a democrat, one under a republican. I think many people are concerned with the upcoming election since the start of the last 2 bear markets where the S&P 500 lost about half its value happened to coincide with an election year (2000 and 2008). Did those years being election years really have much to do with either the tech crash or the housing crisis? Not really. It is more a coincidence than anything else, but being nervous now is understandable if you experienced your account value being halved (or worse) in either of those crashes.

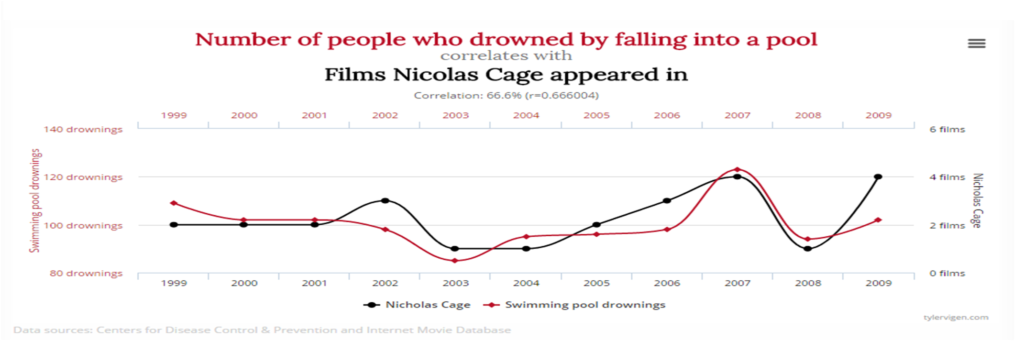

The fact is election years have really not averaged any better or any worse than other years. In election years the S&P 500 has averaged a 10.00% return; for the non election years a near identical 9.99%, according to data from Morningstar. Sometimes people see things that are correlated (meaning when one thing occurs another seems to occur) that have no causation (meaning one thing didn’t cause the other thing). A great example is the number of people drowning in pools overlaid with the number of films Nicolas Cage appeared in.

Based on this graph it might make one think you shouldn’t go swimming for fear of drowning in years Nicolas Cage is in more movies. Clearly, though, the two are unrelated just like the last 2 large bear markets beginning in election years.

If the prospect of an upcoming election is making you nervous about the stock market the issue is not the election or the stock market the issue is how your portfolio is constructed. With a good retirement plan you shouldn’t have to worry about what is going on with politics, the stock market, the economy, etc. since you’d have a plan in place to generate the income you want and need regardless of what is occurring. Many people when they first come in to see us are setup well if the market goes up, but have no plan for or would be devastated if the market goes sideways or down. If you’re in a position like that then you probably should be nervous not only in election years, but pretty much all the time given that markets have fared no better or no worse historically in election years versus non election years.

The fact is no one knows for sure what will happen any given day, month, or year in the stock market. If they did they could become so wealthy they would never have to work again. Everyone can, though, have a plan in place for how they will generate income when financial markets become shaky. If the prospects of a rocky market has you rattled or worried consider speaking with a competent financial advisor that is well versed and focuses primarily on creating tax-efficient retirement income plans that don’t solely rely on the stock market doing well for you to live the retirement you want.

There’s always a reason the stock market could go up and there’s always a reason it could go down. There’s no reason, though, why you shouldn’t have a plan for both.

Material discussed is meant for general/informational purposes and is not intended to be used as the sole basis for any financial decisions, nor be construed as advice to meet your particular needs. Guarantees are backed solely on the claims paying ability of the issuing insurance company. Please consult a financial professional for further information. The S&P 500 cannot be invested in directly and is an unmanaged index of 500 stocks used to measure the performance of US large-cap stocks. Past performance is no guarantee of future results.

Get a plan started with The Retirement Team today by calling 785-228-0222.

Recent Comments